The Zimbabwean commercial real-estate story in 2026 is, surprisingly, a story of nuance. Headline rentals are flat. Vacancy in the Harare CBD remains stubborn. Yet outside the CBD — particularly in suburban office nodes and last-mile logistics — quietly profitable assets are being built and let. This article is a candid snapshot for developers, investors, and family offices considering a Zimbabwean commercial position.

We are construction engineers, not estate agents. Treat what follows as an honest builder's view of the market, not investment advice. Engage a qualified valuer and your tax adviser before committing capital.

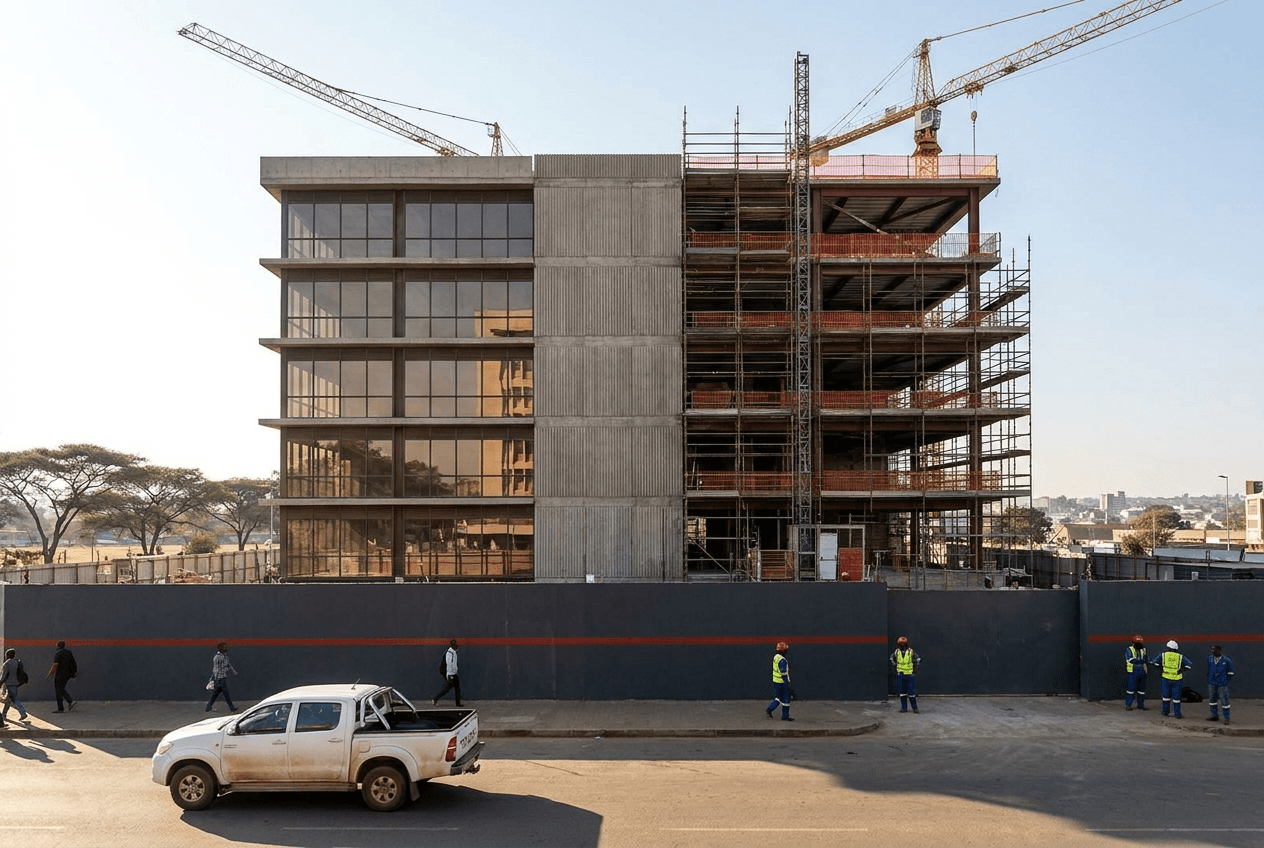

The state of commercial real estate in Zimbabwe — 2026 snapshot

In the broadest terms, here's where rents are landing in 2026:

- Harare CBD Grade A office: $7–11 / m² / month gross. Vacancy 25%+ in many buildings.

- Suburban Grade A office (Sam Levy's, Borrowdale, Highlands): $13–18 / m² / month. Vacancy under 10%.

- Eastlea / Greendale offices: $9–12 / m². Vacancy ~15%.

- Neighbourhood retail anchored by FMCG: $14–22 / m². Vacancy minimal where anchor is in place.

- Msasa & Workington light-industrial logistics: $4.50–7 / m². Demand from regional logistics ahead of supply.

- Bulawayo CBD office: $5–8 / m². Vacancy 30%+. A buyer's market.

The pattern is clear: the CBD is challenged; suburban nodes are healthy; logistics is the surprise outperformer.

The four asset classes performing now

1. Grade-A suburban office

The post-pandemic preference for shorter commutes and cleaner buildings has hardened. Suburban office parks with onsite parking, security, fibre, and backup power are at near-full occupancy at premium rents. The build cost runs $750–$1,100 / m² fully fitted, exclusive of land. Realistic stabilised gross yields land at 9–12%, NOI margins 60–65%.

2. Last-mile logistics

The growth of regional e-commerce, FMCG distribution, and pharmaceutical distribution has created a quiet boom in 1,500–8,000 m² warehouses on the edge of Harare's industrial nodes. Build cost $300–$500 / m². Gross yields 11–14%. Demand exceeds supply.

3. Neighbourhood retail anchored by FMCG

A 1,500–3,000 m² strip centre with a recognised FMCG anchor (Pick n Pay, OK, TM, Spar) and 6–10 small-tenant units around it. The anchor lease (15+ years, USD-denominated, periodic CPI uplifts) gives the asset bankability. Yields land at 9–11%.

4. Small-format mixed-use (5–8 storey)

A new asset class taking hold in nodes like Avondale, Eastlea, and Newlands. Ground-floor retail or food-and-beverage, three to five floors of office or co-working, sometimes two top floors of serviced apartments. Build cost $1,000–$1,500 / m² depending on finish. Yields 8–10% but with optionality across multiple income streams.

The cost of building commercial in 2026 USD/m²

Honest ranges for a contractor's all-in cost (excluding land, professional fees, finance):

- Single-storey logistics warehouse: $280–$450 / m².

- Mid-spec suburban office building: $700–$1,000 / m².

- High-spec suburban office (Grade A finishes, full backup power, fibre): $1,000–$1,500 / m².

- Neighbourhood retail with anchor: $750–$1,000 / m².

- Small-format mixed-use: $1,000–$1,500 / m².

- Grade-A CBD office (rare new builds): $1,400–$2,200 / m².

Specialist items — backup power solutions, water reticulation in nodes without ZINWA, fibre-to-tenant — can add 8–15% on top of these figures.

The yield maths

A simple worked example. Suburban Grade A office, 2,500 m², built on owned land.

| Item | USD | |---|---| | Build cost ($950/m² × 2,500) | 2,375,000 | | Professional fees (8%) | 190,000 | | Statutory & utilities | 120,000 | | Contingency (10%) | 270,000 | | All-in development cost (excl. land) | 2,955,000 |

Stabilised income:

| Item | USD | |---|---| | Lettable area (assume 88% efficiency) | 2,200 m² | | Achieved rent ($14/m²/month) | 30,800 / month | | Gross annual rent | 369,600 | | Operating costs (assume 30%) | (111,000) | | NOI | 258,600 |

Gross yield on cost (excl. land): 258,600 ÷ 2,955,000 = 8.8%.

Add land at, say, $600,000, and yield drops to 7.3%. Net of capex reserves and taxes you are realistically looking at a 6–7% net cash-on-cash yield. Acceptable for a long-hold investor with a stable tenant, less so for a speculative play.

The regulatory path

A commercial build in Harare follows roughly this sequence:

- Town-planning consent. Confirm the existing zoning permits the proposed use. If a special consent is needed, budget 4–9 months and a non-trivial fee. Object-and-appeal processes can extend this.

- EIA (where applicable). Anything industrial, hospitality, or above a certain footprint triggers an Environmental Impact Assessment. Budget 8–14 weeks.

- Building-plan approval. Submission through the local authority. Typical Harare approval times in 2026 run 8–16 weeks for well-prepared submissions.

- Connections. ZESA bulk supply, ZINWA water, sewer connection or onsite waste. These should be applied for during design, not after.

Common rejection reasons: density exceedance, parking ratio shortfall, fire-access non-compliance, set-back encroachment. A good architect catches these before submission.

The build-vs-buy decision

Three quick scenarios:

- Refit beats build when an existing well-located asset is available at a discount to replacement cost (often the case in the CBD in 2026).

- Build beats refit when the existing stock at your target node is functionally obsolete (low ceiling heights, poor MEP, no fibre).

- Buy and reposition when the building is right but the tenant mix is wrong — this is increasingly viable for suburban office assets currently let to weak covenants.

The third option is currently the highest-IRR play we see in the Greater Harare market for capital up to about $4M.

Risk register

A short list of risks every commercial investor should price into the assumptions:

- Currency. USD-denominated leases mitigate but do not eliminate; tenant USD liquidity is the real issue.

- Statutory rate changes. ZIMRA's commercial-property assessments have moved. Track the latest budgets.

- Anchor-tenant dependence. A 70% anchor with a 15-year lease is a feature; a 70% anchor with two years left is a bomb.

- Energy reliability. Backup is no longer optional. Plan for full off-grid capability over time.

- Water supply. ZINWA reliability varies by node. Onsite borehole + tankage is the prudent assumption.

- Construction inflation. Hedged by USD pricing on the build side, but professional fees and labour can drift quickly.

A closing word

We partner with developers on feasibility, design coordination, and execution for commercial assets ranging from neighbourhood retail to nine-storey mixed-use. We do not pretend to be agents or fund managers. We will give you an unvarnished engineer's view of build cost, programme risk, and design optionality.

If you have a site and a thesis, we'd be glad to bring the build.